005: turning nine figs into ten

truly goated gains, 8% over 30 years isn't too shabby, from grocery stores to trading floors

Suppose US$100m landed in your bank account.1

How would you steward this generational wealth?

How would you unlock financial freedom for not just yourself, but also your kids’ and grandkids’ families?

For me, I would start thinking about three things.2

How much gains do I want to make each year?

How much losses can I tolerate before I start selling each year?

How often and how much do I need to turn part of this US$100m into cash?

truly goated gains

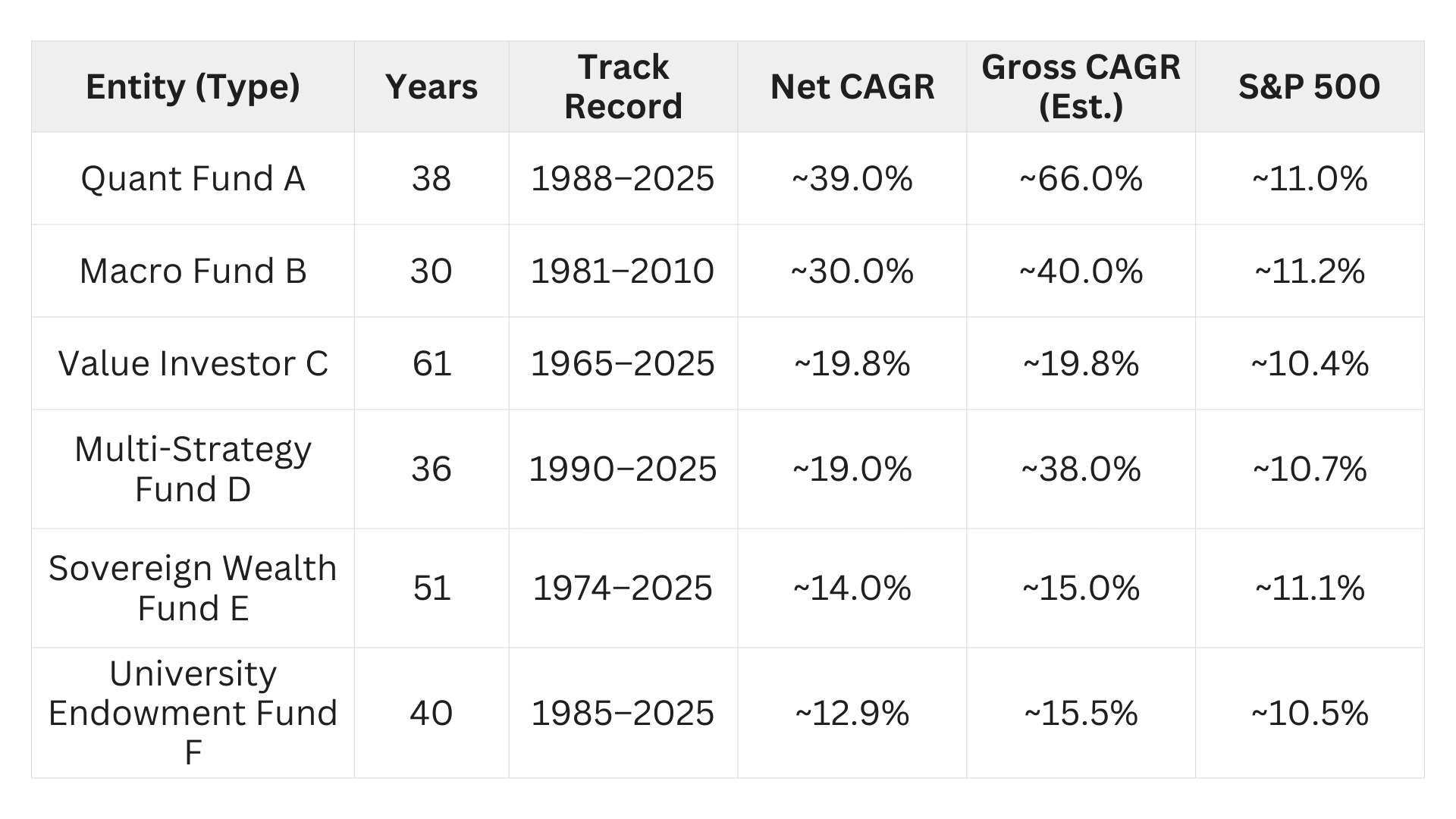

Let’s look at legendary investors who have managed over nine figs for over three decades and did rather well.

I can only marvel at:

How good they were for so long at this game (outperforming the benchmark S&P500 for at least three decades, dating back to the ‘80s);

How much they have made for themselves.

It also makes me slightly depressed knowing:

How much they keep for themselves before making money for others;

How they most likely can’t help me turn my US$100m into US$1bn.3

8% over 30 years isn’t too shabby

Now look, what if I just throw everything into something compounding at 10%.

How much can I make?

Within 10 years, I cannot turn nine figs to ten...

Unless my US$100m grows at 25.89%+ on average each year for a decade straight.

Within 30 years, however, I become a billionaire...

Provided my money grows at 8%+ on average each year for three decades straight.

No wonder Investor C once said ‘The stock market is a device for transferring money from the impatient to the patient.’

from grocery stores to trading floors

Most of us haven’t experienced raging inflation before.

Last year, I met an Argentinian who did.

‘By the time I took an item off the shelf and brought it to the cashier, the price was different.’

‘Grocers were literally shouting out prices, like on trading floor, because the Argentinian peso devalued so rapidly.’

Adjusting for inflation is a must.

So how much gains do I want to make each year?

Personally, I’d go for inflation + 4-6%.

At current PCE levels of 2.8%, that’s roughly 7-9%.

I’m not handing a significant sum to anyone promising mid twenties over the long term. There must be a catch.

We discuss risk next week!

Fully KYCed, unencumbered, post tax. Which is almost never the case.

AKA my return expectation, risk tolerance, liquidity and distribution needs.

A and B are so good at making money they just want to make money for themselves. C has recently retired after over 60 years. D is impossible to access without paying exorbitant fees. E and F cannot make money for people like me who don’t fall within their constituent.

Bitcoin still my bet as a decorrelated inflation hedge and growth asset :)